|

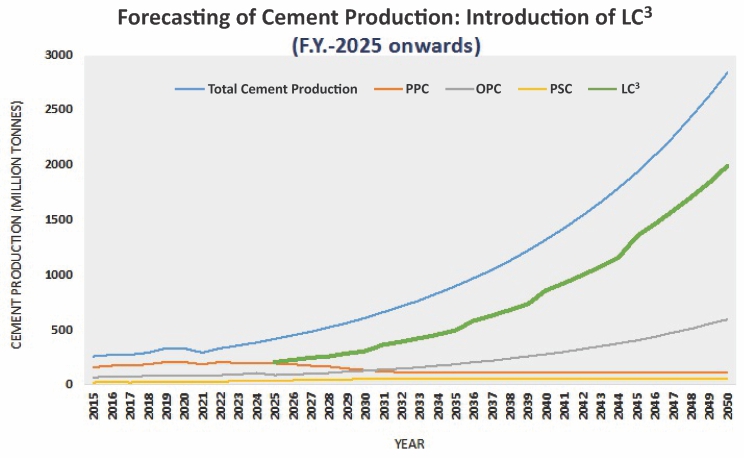

Infrastructure development is widely acknowledged as the key to achieving growth. It has been the primary focus area for the Government of India, and it is reflected in its current policies and plans. The government has set out to achieve ambitious goals of becoming a 5 trillion USD economy by the end of 2024, which is important for the cement industry as it paves the way for infrastructural development and lays the foundation for building a new India (Thomas, 2020). Our country’s cement production is the second-largest globally, with an overall production capacity of nearly 545 million tonnes (MT) for 2020. With the growing population, more reliable infrastructure is becoming an absolute necessity. Apart from that, it is an essential product that is utilised by all industries and forms a solid backbone for advancement and acceleration of socio-economic growth. It provides a large number of direct and indirect employment opportunities, contributing in a big way to the GDP. To continue this positively advancing trajectory, one needs to consciously look out for greener alternatives that can be easily incorporated without disrupting the system. LC3 has the potential to become a greener alternate solution that promises sustainable growth in terms of economies, ecological stewardship, shareholder value creation, and community well-being worldwide. It reduces carbon dioxide emissions up to 40% as compared to ordinary portland cement. That is possible due to the change in the composition of the raw materials, as LC3’s primary raw material is 40–65% clinker, 30–38% calcined clay, 15% crushed limestone, and 7% gypsum. It utilises lower grade clay, which is usually abandoned and left to the agents of erosion, thus creating value. Additionally, the energy requirement for calcination in LC3 production is half of what is needed to manufacture ordinary cement. Because of the softer nature of materials, necessary power required for grinding is reduced, making it more cost-effective to produce. It is a development that could gain momentum quickly due to high availability of limestone and low-grade clay in India. It does not require capital-intensive modification in existing plants. The accompanying graph visualises the production trend for different varieties of cement, along with the introduction of LC3 in 2025.

Source: Author’s analysis At the 26th Conference of Parties (COP26) held in Glasgow in late 2021, Prime Minister Narendra Modi promised that India would achieve net-zero emission by 2070. In the meantime, our government also pledged to meet immediate goals, which would help in facilitating the larger target. Among the immediate goals for 2030 are receiving assistance to increase India’s non-fossil fuel energy capacity, meeting 50% of the country’s energy requirement through renewable, reducing CO2 emissions by 1 billion tonnes, and bringing down the carbon intensity of India’s economy by more than 45%. Reaching these momentous milestones would enable India to pave a firmer path towards decarbonisation. It would eventually lead India to emerge as a world leader, not just in taking action but also in creating technology and finding low-cost alternatives for the adaptation-related issue, which is looming today. Keeping in mind the points mentioned above and our team’s progress with LC3, we at Development Alternatives approached the Director of the Ministry of Mines, Vivek Kumar Sharma. Our discussion there was extensive, and we gained insights into the organisation’s working. While LC3 is our best possible alternative to mitigate emissions, its large-scale adoption is highly dependent on how the governmental nodal organisations incorporate it into various policies not only to make it mandatory for the cement manufacturers but also to increase its social acceptance. For increasing awareness and social acceptance of alternative cement, government infrastructure and public sector undertaking (PSUs) would be ideal testing grounds. That can provide impetus to the public at large to adopt such greener alternatives. Supporting the transition of domestic cement manufacturing to low-carbon cement would ensure that the sector would keep 0.54 million jobs in 2050 and zero import dependency on the limestone imports (Biswas, Ganesan, & Ghosh 2019). References:

Sumedha Singh |